-

Protecting Millions from Silent Financial Traps

Weekly blog #34. Protecting Millions from Silent Financial Traps. A recent policy direction on regulating online real-money gaming reflects how pro-people governance can protect society at large. With participation crossing 40 crore users, many – especially from economically weaker sections – were getting drawn into high-risk platforms that often led to financial distress, family breakdowns,…

-

A Model to Address Inequality — My Article on the Julius Baer Foundation Knowledge Hub

Inequality remains one of the most persistent challenges in modern economies. In this article, I present a model that attempts to address structutal gaps through a more direct and targeted approach. The framework builds on the idea of aligning resources more efficiently with those who need them most. The full article can be accessed here:…

-

Notes on Inequality#11. Formal vs Informal Divide

The rollout of GST was a necessary reform for bringing transparency and uniform taxation. GST accelerated formalisation, though not without challenges. It has unintentionally widened the gap between formal and informal sectors. Many MSMEs, especially micro units, struggle with compliance, invoicing, and filing requirements. Unable to fully utilize input tax credits, they face cost…

-

Notes on Inequality #10. When Equality Hides Inequality.

Sometimes, “more equal” means “similarly struggling”. Or, we can just say, when everyone is equally poor, the data calls it “equal”. Reason why, the Gini Coefficient which measures inequality, does not always reflect the true picture. The Gini coefficient ranges from 0 to 1 – where 0 means perfect equality ( everyone earns the…

-

Notes on Inequality #9. When Prices Rise, Inequality Deepens Silently.

When Prices Rise, Inequality Deepens Silently. An important but often overlooked driver of inequality is inflation. It does not affect everyone equally. Fixed- income earners – salaried individuals and pensioners – face a steady erosion in purchasing power as prices rise. In contrast, borrowers and many businesses often benefit, as they repay debt with devalued…

-

₹166 lakh crore in 1688 hands — can ₹7 lakh crore a year change India’s future?

Weekly Blog # 33. ₹166 Lakh Crore in 1688 Hands – Can ₹7 Lakh Crore A Year Change India’s Future? Between 2019 and 2025, India has witnessed an extraordinary surge in wealth at the very top. Individually, even figures like Gautam Adani saw their wealth rise by an astonishing 625%. Entrepreneurs are valuable assets to…

-

Notes on Inequality#8. An Economy Grows Strongest Where Credit Reaches the Smallest Hands.

In my last notes, I spoke about inequality in land and representation. But inequality also exists in something less visible – access to credit. For millions, the challenge is not lack of effort or intent, but lack of access. Financial inclusion begins where credit inclusion ends. In the formal system, credit is often linked…

-

Notes on Inequality#7. A Small Piece of Land Can Change a Family’s Destiny.

A Small Piece of Land Can Change a Family’s Destiny. Reform the land, reshape the future. A recent report by World Inequality Lab highlights a stark reality : the top 10% of landowners in India control nearly 44% of agricultural land, while the top 1% alone hold 18%. This imbalance is not just about…

-

Notes on Inequality#6. Education vs Business? The Line is Blurring

Education or Business? The Line Between Learning & Profit is Blurring. Rising privatization in education has quietly widened the gap between the affluent and economically weaker sections of society. Many private institutions today function increasingly like commercial enterprises – high fees, selective admissions, and brand-driven pricing. Institutions with strong reputations command even higher fees,…

-

Notes on Inequality#5. Fair vs Unfair Inequality.

Not all inequality is the same. Fair inequality rewards effort, skill, and innovation. The outcomes differ despite equal opportunity – for example, two equally educated individuals earning differently based on skills and effort. Unfair inequality arises from unequal access, privilege, or bias – where opportunities are limited and outcomes are skewed, regardless of merit or…

-

A ₹2 Lakh Policy Cannot Replace a ₹40000 Monthly Income. Then Why Do We Still Buy?

Weekly Blog #32. Over the years, I’ve seen one pattern – families often realise too late that their ‘insurance’ wasn’t enough. Insurance is not about returns – it is about income replacement. Take the case of Ashok, 35, the sole earning member of a family of six – wife, two young children, and retired parents.…

-

Notes on Inequality#4. Is Inequality Needed For Growth?

But evidence does not clearly support this. Growth does not need inequality – it needs opportunity. Growth built on exclusion is fragile; growth built on inclusion is durable. Countries like South Korea focused on education and broad access, lifting millions into the middle class. Norway shows that prosperity can be sustained with low inequality.…

-

Notes on Inequality#3. The Cost of Not Understanding Money.

The Cost of Not Understanding Money A small financial mistake for the privileged is a lesson. For the vulnerable, it can become a lifetime setback Missing an EMI, taking a high-interest loan, or falling for financial traps – these are not just errors. They have consequences that compound over time. Financial Literacy is often seen…

-

Notes on Inequality#2. When Money Overrides Merit

Notes on Inequality#2 When Money Overrides Merit. When education has a price tag, merit becomes optional. Seats go to those who can pay, not always to those who deserve. The result? Compromised professionals and a system that rewards privilege over potential. A system that sidelines merit eventually sidelines its own future. Inequality doesn’t just grow…

-

Notes on Inequality #1. In Every Crisis, Inequality Finds a Way to Widen.

The greatest irony of war? It punishes those who neither start it nor benefit from it. Developing countries absorb the shock. The poorest within them absorb the pain. And it doesn’t stop at war. Floods, droughts, storms – every crisis follows the same script. Uncertainty is not neutral. It amplifies inequality. Or, we can say,…

-

Notes on Inequality ..a new series

Starting Something New….. I have been reflecting on small, everyday aspects of finance, economics, and inequality – often subtle, but deeply impactful. I thought of capturing these as short, crisp pieces under a series : “Notes on Inequality”. Alongside my regular weekly posts, I’ll be sharing these brief thoughts from time to time. These notes…

-

An Unequal World is an Unstable World

With this 31st post, I reflect on a growing global concern. A recent insight from EQUALS highlights a striking reality: 3428 billionairs now control $20.5 trillion, with their wealth increasing by $4 trillion in recent years – more than the total wealth of the poorest 4.1 billion people combined. This is not just a…

-

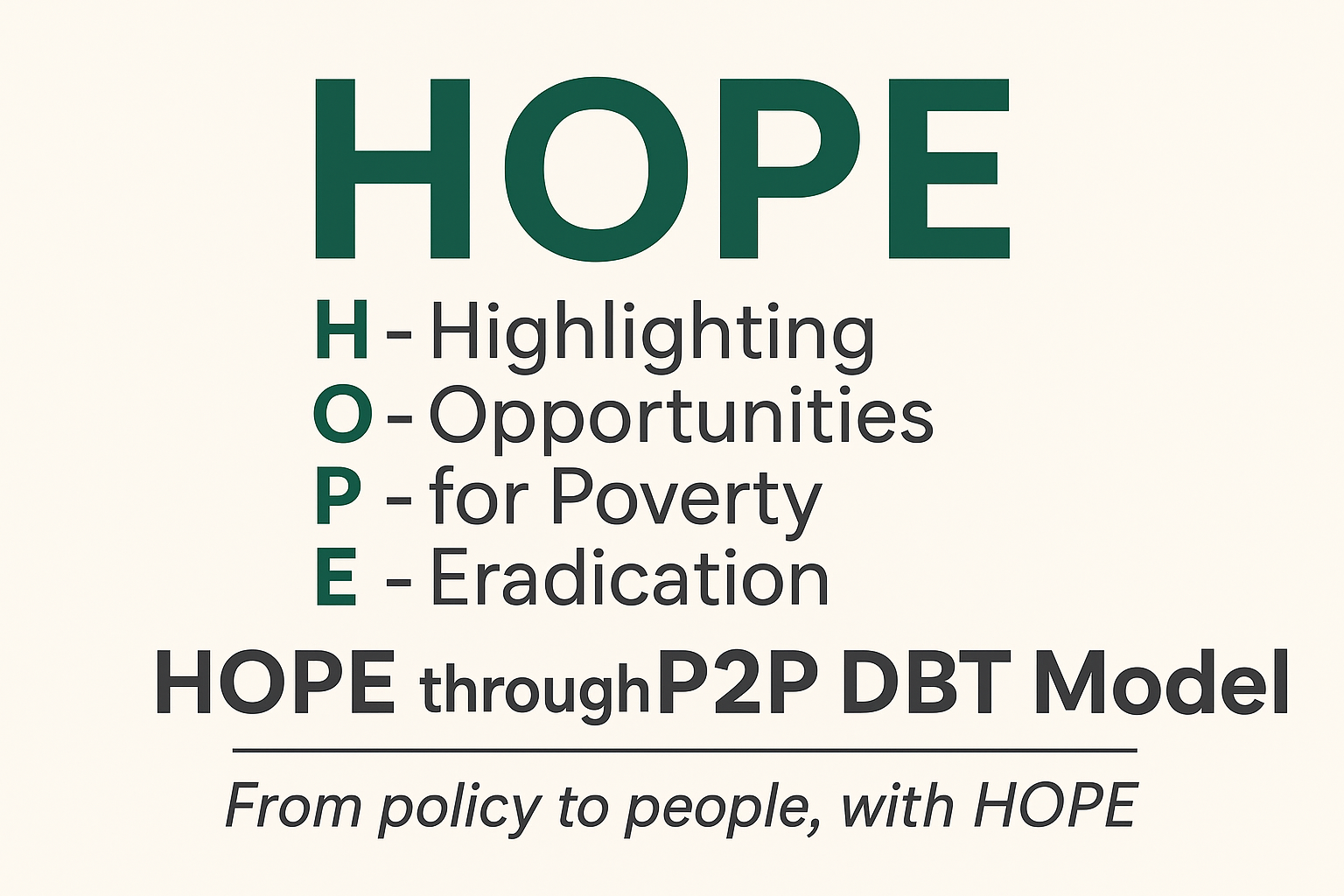

Between Reality and Change Lies Hope.

As this series reaches its 30th post, I reflect on hope — the human foundation behind meaningful change. Highlighting Opportunities for Poverty Eradication [ HOPE ]. The P2P DBT Economic Model is a proposed framework designed as a ‘bridge’ to HOPE. How it works: • Government-verified beneficiaries mapped through an App (like Google Maps) with…

-

Pay 2 extra EMIs. Save 6 years.

Most home loan borrowers focus only on EMI – but a small tweak can save you years. Suppose, you take a ₹40 lakh home loan at 8% for 20 years. Your EMI comes to around ₹33460. Like most loans, a large portion of your early payments goes toward interest. Now, consider a simple strategy :…

-

Financial Stress is Common, But it Shouldn’t be Normal

Financial Stress : The Silent Productivity Killer in the Workplace. Financial stress rarely shows up in official reports, yet it quietly erodes productivity in many workplaces. An employee may appear present, but mentally they could be worrying about credit card dues, personal loans, medical emergencies, or an uncertain financial future. When financial anxiety occupies the…

-

Citizen Participation Layer for India’s Digital Public Infrastructure

Citizen Participation Layer for India’s Digital Public Infrastructure. India has built one of the world’s most robust digital public infrastructures. The digital stack already includes several foundational layers: 1. Identity Layer – Aadhaar-based digital identity enabling reliable authentication. 2. Payments Layer – Real-time payment systems such as UPI and AePS built by the National…

-

The easiest way to grow is to reduce financial leakage

Your first investment return is the interest you stop paying. According to the latest Financial Stability Report of the Reserve Bank of India (September 2025), over 55% of Indian household debt is now non-housing related. Even more concerning – related debt has nearly tripled in just five years. We are increasingly living on borrowed future…

-

High PE isn’t expensive if growth justifies it. Enter PEG.

When we invest in shares, we should not just see the price – we should ask whether the price makes sense. Price should reflect performance, not excitement. The PE ratio (Price to Earning ratio) tells us how much investors are willing to pay for ₹1 of a Company’s profit. Formula : PE=Share Price/ Earning Per…

-

Rethinking Welfare Architecture

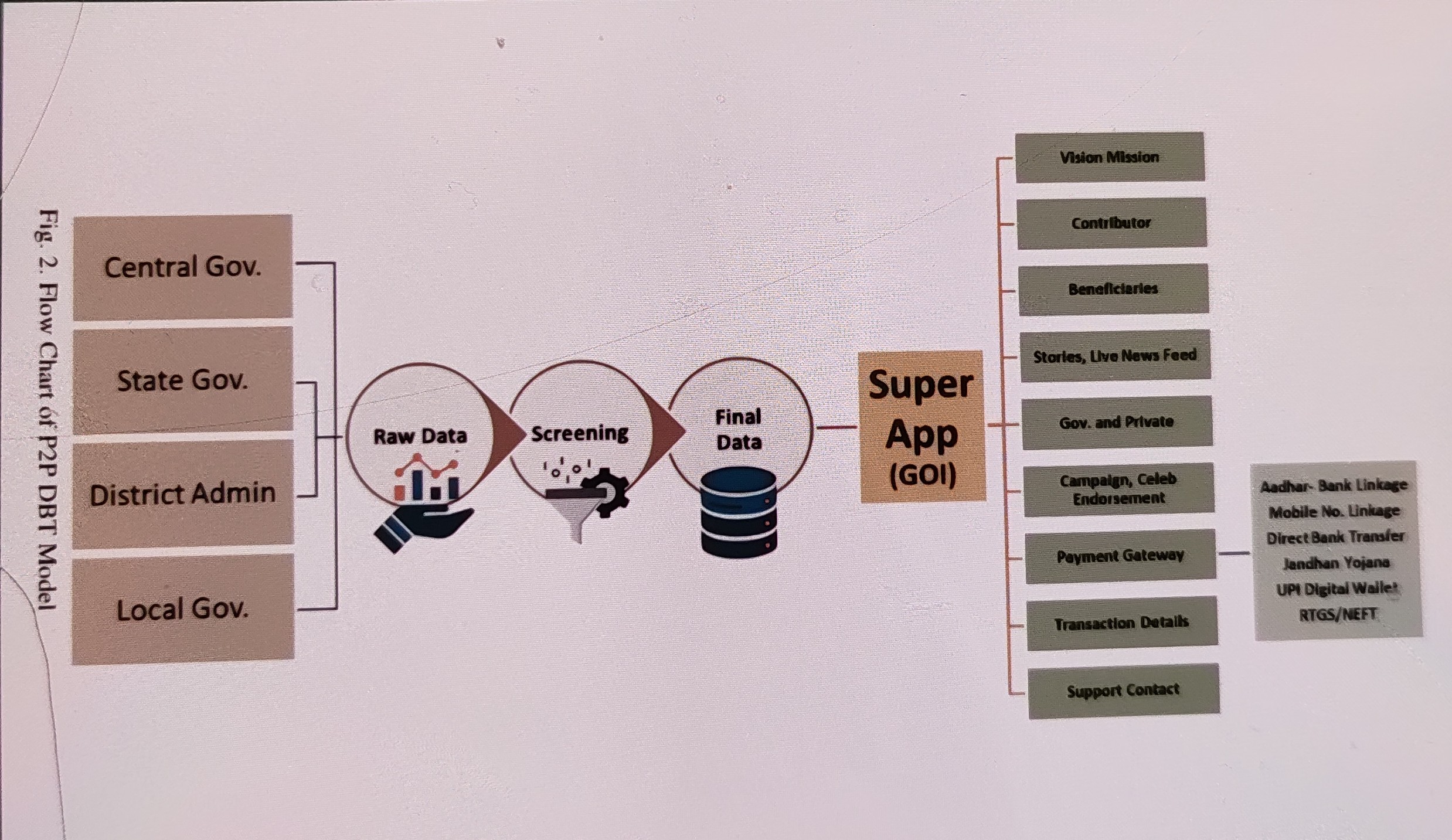

Rethinking Welfare Architecture Across India several states are expanding Direct Benefit Transfer (DBT) schemes to improve social security and inclusion. The intent is commendable. However, support should ideally be based on poverty, vulnerability and genuine need — not blanket distribution. This is where P2P DBT — a complementary economic model I have conceptualised, becomes relevant:…

-

Understanding NAV & INAV: Why?

Understanding NAV and INAV : Why? With the growing popularity of ETFs – especially Gold ETFs – many retail investors are entering the market without fully understanding how ETF pricing works. One concept that often gets overlooked is the difference between NAV and INAV. Ignoring this difference can mean unknowingly buying an ETF at a…

-

When Forced Savings Disappear — The Hidden Cost of New Tax Regime

The new tax regime promises simplicity – lower rates, fewer deductions, less paperwork. For many taxpayers who don’t fall into higher tax brackets, it appears attractive on the surface. But beneath this simplicity lies a subtle, long-term concern that deserves attention: the gradual erosion of savings discipline. Under the new tax regime, the absence of…

-

P2P DBT — A Model for Poverty Eradication

Over the past several months, this blog has focused on personal finance, resulting in twenty write-ups exploring individual financial decision-making. Alongside this, a P2P framework has been outlined under a separate section of the blog. In this post, I begin analysing the framework from different perspectives – how it could function in practice and how…

-

“Mutual Funds Sahi Hai” — but, to what extent?

“Mutual Funds Sahi Hai” is one of the most familiar financial slogans in India today. It has created awareness, curiosity, and participation among millions of investors. But, an important question remains: Is it really “sahi” for everyone ? And if yes, to what extent? The answer is not a simple yes or no. Mutual funds…

-

Before Chasing Returns, Fix Your Allocation

In my previous blog(18th), I emphasized the importance of identifying your risk profile – this is how you can assess how much volatility in the market you can withstand – both financially and emotionally. Asset allocation is a direct outcome of that understanding. For example, two investors of the same age may have different…

-

Know Your Risk Profile Before You Invest

Understanding Your Risk Profile: The Most Ignored Step in Investing. The right portfolio begins with the right risk profile. To be more specific, investing starts with self-awareness. When people talk about investing, the discussion usually revolves around returns – how much can I earn, which asset is performing best, or which stock gave multi bagger…

-

Buying Your Home? Calculate Time, not just Price.

I had an interesting experience while accompanying a close friend and his family to Mira Road in February 2024. They were exploring the option of investing in a 1 BHK flat in an under-construction project by a reputed builder. On the surface everything looked promising – an upcoming metro line, close proximity to the Western…

-

The Magic of Compounding

The Magic of Compounding : Small Steps, Big Wealth. Compounding is often called the eighth wonder of the world. The idea is simple: when your money earns returns, your wealth grows at an accelerating pace. It feels slow in the beginning, then suddenly powerful – almost magical. So, when time becomes your business partner, magic…

-

Understanding Ponzi Schemes : The First Step To Financial Safety

Every scam starts with a sweet promise. Don’t bite. In today’s fast-paced world, everyone is looking for ways to grow their money quickly. Social media is filled with stories of people doubling their investments in a few months, and advertisements promising “guaranteed returns” pop up everywhere. But behind the glitter of easy money often lies…

-

Retirement is Earned Over Years — Begin Your Journey Now

Planning your retirement starts with one big question : “How much money will I need when I stop working?” The amount you need is called your retirement corpus. Calculating it is easier than it appears if you follow a step-by-step approach. Step1. Estimate your monthly expenses after retirement. Start by identifying how much you…

-

The Risk of Living Too Long

The Risk of Living Too Long! In my 3rd Blog, I discussed the importance of life and health insurance. Insurance acts as a shield, protecting our family from unforeseen events that could push them into financial distress. That is essentially the risk of dying too early. When we think about risks in life, the mind…

-

The Seven Rules That Saved Me from Trading Losses

As a financial planner, it may sound unusual for me to write a blog on trading. But the reason I’m doing so is simple – my job is to ensure that you don’t fall victim to reckless day trading and end up making holes in your hard-earned wealth. Disciplined and well-informed trading is absolutely…

-

The Day You Stop Chasing Money

If you’ve visited my blog, you’ve surely seen that banner – birds breaking free from their chains.That wasn’t a random pick! It’s a quite reflection of what financial freedom means to me: The power to rise above worries and fly on your own terms. That’s exactly what today’s post is all about. Everyone dreams…

-

When The Market Lies — Check The Book Value

When The Market Price Lies – Check The Book Value In my previous blog, we discussed how to analyse a stock through its earnings, PE and PEG – the core pillars of fundamental analysis. Now, let’s take one step further and understand another crucial measure – how to value a share based on its Book…

-

Valuing a Share — The Easy Way to Begin

Every company tells two stories – one through its profits and the other through its worth or value. The profit story builds your EPS ( Earning Per Share) and PE ratio ( Price Earning ratio); the worth story builds your Book Value and PB ratio (Price to book). Smart investors learn to read both…

-

Equity Rewards The Brave — Safety Has It’s Cost

Equity Rewards The Brave – Safety Has Its Cost If someone had told you in 2003 that a ₹10,000 investment in a watch company would become ₹18.2 crore, you’d probably laugh. But that’s exactly what long term equity investing can do. This is the story of Titan, a Tata Group Company. There are so many…

-

Financial Yield Matters

Why Financial Yield Matters in Investing. I’ve received a few suggestions that I should occasionally switch to more practical and relatable topics, instead of making the series feel like a textbook. Point taken! I completely agree – my goal has always been to share fresh, useful concepts that can genuinely help you make better financial…

-

The Four Pillars of Investment

The Four Pillars of Investment: What Every Investor Must Know Investment simply means putting your money into something with the expectation of earning a return in the future. Instead of keeping cash idle, you make it work for you. For example, if you deposit ₹10,000 in a bank fixed deposit at 6% interest, it will…

-

Credit Card : The Dark Side of Plastic Money

Credit Card : The Dark Side of Plastic Money In my last post, I talked about setting financial goals – the road-map that helps you save, invest and plan for a secure future. But even with the best plans, there are pitfalls that can silently derail your progress. One of the most common traps? Credit…

-

Financial Goal Setting

Financial Goal Setting: The Foundation of Your Money Journey.Think of financial goals as your Google Maps. You first decide where you want to go, then choose the best route to reach there. In money matters, too, clarity of goals leads to clarity of action. Step 1. Define What Matters To YouFinancial goals are deeply personal.…

-

Adequate Protection – Life & Health Cover Before Setting Goals

I thought of writing about goal setting in today’s blog, but I changed my mind to discussing adequate insurance cover. Protection comes before planning, because without it, unexpected events can derail even the best financial plans. Suppose, you have set your financial goals. If life goes smoothly, you are likely to achieve most of them.…

-

Emergency Fund

Start with an Emergency Fund Before Anything Else. Before you dive into financial planning, the very first step you must take is to build a solid emergency fund. Why? Because life is unpredictable. An emergency fund gives you the financial cushion to deal with sudden shocks – be it job loss, a medical emergency or…

-

Habit of Saving : The Foundation of Financial Well- Being.

“ We are what we repeatedly do. Excellence, then, is not an act but a habit. “ — Aristotle The same applies to money. Saving is not a one-time act; it’s a habit. And the earlier you start, the stronger your financial foundation becomes.